So much to blog about, so little time. From Inman News: "The housing market is now the all-consuming economic topic, and ‘prices are falling’ is the everybody-says, everybody-knows factoid du jour. It’s not a whisper-turns-to-hysteria deal. The dominant tone in the prices-are-falling pronouncement is pleasure, often self-satisfied and/or envious: I knew they would fall. Serves ’em right (most common among those who missed the party, couldn’t afford to buy what they thought they deserved, or don’t much care for Realtors).

So much to blog about, so little time. From Inman News: "The housing market is now the all-consuming economic topic, and ‘prices are falling’ is the everybody-says, everybody-knows factoid du jour. It’s not a whisper-turns-to-hysteria deal. The dominant tone in the prices-are-falling pronouncement is pleasure, often self-satisfied and/or envious: I knew they would fall. Serves ’em right (most common among those who missed the party, couldn’t afford to buy what they thought they deserved, or don’t much care for Realtors).

Seller gets zillowed and plans to sue. read

Nightmare mortgages foil the American Dream. read

Map of misery. see

Toxic mortgage ha ha. see

{kind=link}

Appreciation erosion significant. read

How to profit in a slow economy. read

Grand Sierra and Montage execs interviewed. watch

Think our market’s bad? Check this out. read

Odd Todd’s interest only loan implodes. watch

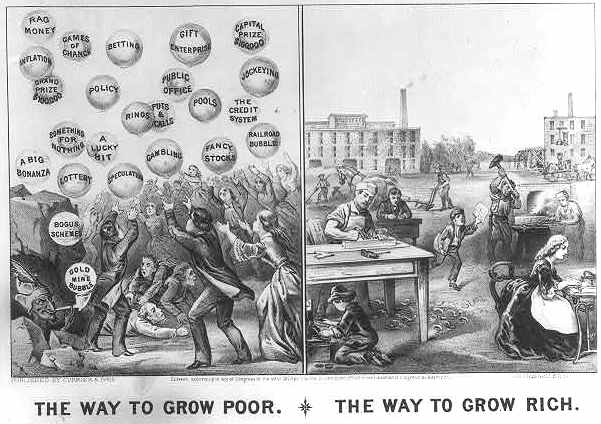

Bubble picture from the past. see

{kind=link}

Asset depletion imminent. read

10 Responses

Diane, When might we expect your monthly report on market activity for August?

The “Map of Misery”

So 1 out of 5 buyers in Reno has purchased with an option ARM. The only reason anybody uses an option ARM is because it is the loan that allows for the lowest possible initial payment. It is the loan that allows the least qualified buyer to purchase the largest possible house he cannot afford. It is the most deadly of all the suicide loans.

Ninety percent of all borrowers who take out option ARMs make only the minimum payment, which does not even cover accruing interest, let alone reduce the principle balance. Once the unpaid balance of the loan grows to a designated amount, the loan resets. This typically occurs 18 or 20 or 24 months after origination. When it resets, not only is the total unpaid balance higher, but the interest rate jumps to prevailing rates. The borrower, who took out the loan in the first place because it was the only way he could “make the payment”, now sees the monthly payment as much a triple. Say goodnight.

In addition to all the other sellers who will elect to place their house on the market in the coming year or two, we can look for the houses of 1 in 5 of all recent purchasers to also come on the market. By foreclosure or otherwise.

Indeed, if one seeks to lock in declining value in Reno, there has never been a better time to buy.

Check out these 2 listings:

MLS# 60021139

MLS# 60022622

They have the same address and same APN. The former was withdrawn earlier today and the latter was newly listed a short time later, at a lower price. The original listing is at DOM: 18. At first the new listing stated DOM: 1, but now it says DOM: 8. Obviously, the Reno MLS can not be trusted.

-EyesWideOpen

My bad, it’s still DOM: 1.

Eyes: # 60022622 is the Montage listing that just went up recently. It features a 600 sq. ft. studio at the bargain basement price of only $410 a sq. ft.

Pretty much got to go to Montreux to beat that on a per sq. ft. basis.

Let’s see. You could buy it with a nothing down interest only loan at 6% for $1400 a month. Just for interest. Add to that taxes at say $230 a month, and who knows what for the HOA fee, another $250?

So for only $1,880 a month, more or less, you could live in a 600 sq. ft. studio without even a bedroom.

But it would be in Reno’s only “urban village.”

Dagnabit! My bad again. Sometimes I keep too many windows open at once.

I double-checked the numbers this time. Please take a look at these and then tell me why this practice is allowed.

Same address, same APN:

60021139 – Withdrawn – DOM: 18

60022615 – Relisted – DOM: 1

Eyes: # 60022615 is a studio in the old Comstock Hotel now known as the Riverwalk. Here you can get 394 sq. ft. for the bargain basement price of only $380 a sq. ft.

It appears that the Riverwalk, not being an “urban village” like the Montage, is relegated to being $30 a sq. ft. cheaper.

As far as DOM goes, why would you think overpriced condo listings would be any more reliable than SFR listings?

So the housing bubble bursting is now the cover story for Business Week.

snip…

After prolonging the boom, these exotic mortgages could worsen the bust. They also betray such a lack of due diligence on the part of lenders and borrowers that it raises questions of what other problems may be lurking. And most of the pain will be borne by ordinary people, not the lenders, brokers, or financiers who created the problem.

snip …

Forgot to add that I was told by an unemployment worker that a mortgage company employee was in there seeking employment help after a local mortgage company had laid off several people. This worker shared that she was forced to push people into loans they could not afford or lose her job. Hmmmmmm.

Hey Diane your last couple of sentences are right on the mark. After cruising around many real estate info sites, most comments are extremely negative and seem to be from people who did not buy when prices were cheap. These are the types who can only bring themselves up by anothers misery. However that will not help them in their belief and wanting that home prices will return to 2001 prices.